German (DE)

German (DE)  English (US)

English (US)  Spanish (ES)

Spanish (ES)  French (FR)

French (FR)  Hindi (IN)

Hindi (IN)  Italian (IT)

Italian (IT)  Russian (RU)

Russian (RU) ![]()

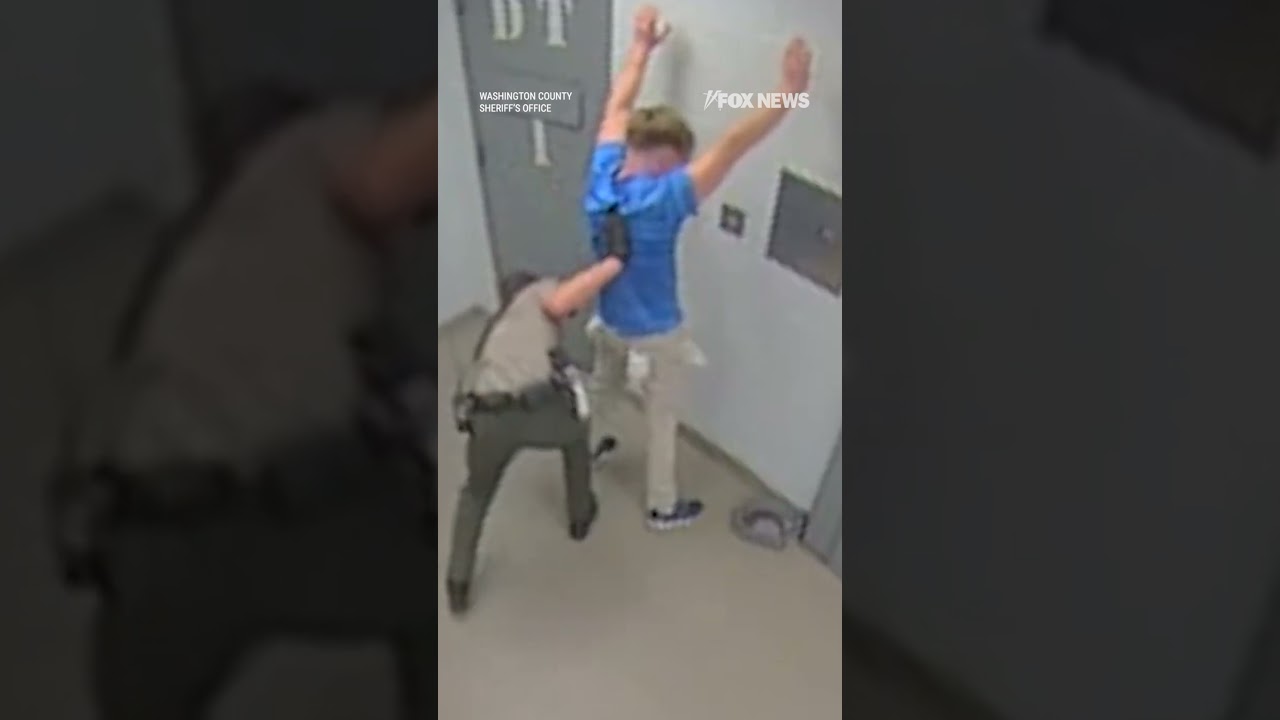

On Friday morning the Bureau of Labor Statistics released disappointing jobs numbers. A few hours later, President Trump announced that he was directing the administration to fire the commissioner responsible for this highly respected, nonpartisan agency, widely considered the producer of the best labor market data in the world. This is closer to what one expects from a banana republic than from a major democratic financial center.

This is even more senseless than his other threats to fire officials like Jerome Powell, the chairman of the Federal Reserve. Powell makes consequential policy decisions (and as I have written, there is very good reason to insulate him from political pressure).

Erika McEntarfer, the fired B.L.S. commissioner, is a highly respected economist with extensive experience in the production and analysis of government data. But she does not make policy in the way that someone like Powell does. Nor does the commissioner traditionally even make the particular numbers that the B.L.S. releases. Instead those numbers are produced by the 2,000 nonpartisan career staff members who work in the agency, in this case compiling the survey responses from the more than 100,000 businesses that report their employment to the B.L.S. every month. The numbers are finalized before they get to the commissioner, a political appointee but one who often serves across administrations. The role is much more about managing and overseeing the agency and making long-term decisions.

Trump’s ire was directed at the large revisions to the May and June jobs numbers, which went from a previously reported respectable average of 145,500 new jobs per month to a more concerning 16,500. The revisions were unusually large — the largest since 1979, not counting the pandemic, according to economist Ernie Tedeschi.

But revisions are a normal part of the statistical process and, in fact, one of its strengths in balancing timeliness and accuracy of data. About one-third of the sampled businesses do not return their survey responses on time, so the initial numbers have to make imputations for the missing data. As more survey responses arrive at the B.L.S., the numbers are revised. In addition, the B.L.S. is constantly using an algorithm to do updated seasonal adjustment of its data (e.g., the normal pattern of hiring a lot of retail workers in November and December and laying them off in January); this algorithm was a major factor in the latest revision.

In his post, Trump accused the B.L.S. of having “manipulated for political purposes” the numbers. Not only is that claim far-fetched; it is also internally contradictory. The B.L.S. produced some large downward revisions of jobs numbers under President Joe Biden, too. The revisions were slightly different from these, because the Biden ones were part of an annual revision process using more reliable tax data. But Trump argued then that Biden helped himself by cooking the books by initially reporting high numbers, which were revised downward in August 2024.

Trump alluded to that claim on Friday. In the same post, he argued that the B.L.S. is also hurting him by initially reporting high numbers but then revising them downward. The same action couldn’t have helped Biden and hurt Trump.

And, ironically, the latest revisions strengthen Trump’s arguments for the Fed to restart its rate cuts.

The firing of the B.L.S. commissioner is more senseless than the threat of or actual firing of the Federal Reserve chairman, though not as consequential. But it still matters. Policymakers like the Federal Reserve Board members need reliable data — as do financial markets, including investors lending the United States trillions of dollars to finance our huge budget deficits, and businesses making decisions. Faked data in countries like Greece and Argentina helped enable bad policies and played a role in the economic crises they suffered this century.

The good news is that any appointee in this system, from good ones to bad ones, is just one person in a 2,000-person, highly technocratic, nonpartisan agency, who would have a hard time faking the data. The bad news is that it is not impossible to corrupt data. And either way, the confidence investors and the public have in the data could suffer a serious and senseless blow.

![]()

President Trump inherited an economy in excellent health, and the predictions that he would quickly cause a recession were wishcasting rather than forecasting.

But Trump has been doing his level best to disrupt the American economy, and in the latest batches of economic data, there are signs that he is having an impact.

Trump’s big economic idea, of course, is to reduce the amount of stuff that Americans buy from the rest of the world by imposing hefty tariffs, or taxes, on imports. Trump himself has acknowledged that this will cause some short-term pain, but he says that it will be worthwhile because it will produce a boom in domestic manufacturing.

So far, Americans are experiencing some costs but not the purported benefits.

Over the last three months, after revisions, the American economy added about 106,000 jobs — or less than a third of what is needed to keep pace with population growth. It’s the weakest three-month stretch since 2020, and there’s even more reason for worry in the details. While the unemployment rate remains low, at 4.2 percent, that is because a growing share of Americans aren’t even trying to find jobs. If the share of adults either working or looking had held steady over the last three months, the unemployment rate would be at almost 5 percent.

The latest jobs data includes a sharp downward revision in estimated job growth in May and June as well as a relatively weak number for July, underscoring that predicting economic trends is a perilous business. We’re only beginning to get a clear picture of the first half of this year, let alone what’s going to happen next.

But wobbly job growth isn’t the only sign of increasing stress. Overall economic growth appears to have slowed in the second quarter and there are signs that tariffs are beginning to bite. The latest inflation readings, for June, showed that prices are rising a little more quickly. Consumers, the engine of the economy, are still spending, but at a slower pace than last year.

And what of Trump’s new economy? Well, that’s the worst news of all: Friday’s jobs report showed that manufacturing employment declined for the third straight month.

And what of the president? He responded to the bad news about jobs by trying to punish the messenger: He announced that he had directed his team to fire the head of the federal agency that compiles the employment numbers, a decision that threatens to undermine public confidence in the accuracy and integrity of federal economic data.

The economist John Maynard Keynes said that when the facts contradicted his opinions, he changed his mind. This president prefers to change the facts.

![]()

If President Trump tries to fire the Federal Reserve chair, Jay Powell, it will not end the Federal Reserve’s independence overnight. But nor will refraining from trying to fire Powell before his term ends in May 2026 guarantee the Federal Reserve’s continued independence.

The Fed was carefully designed to resist short-run political pressures, but it may be defenseless against a sustained and patient effort to undermine that independence over the course of two presidential terms. While I abhor the thought of Trump firing Powell, in some ways I am even more worried he might surprise us and show the patience to start that sustained transformation process by nominating a politically pliant hack to the job next year.

Federal Reserve independence is the closest thing to a free lunch that macroeconomists have identified. Decades of research and experience in the United States and around the world has shown that when central banks are protected from political interference, they deliver lower and more stable inflation without any losses in terms of unemployment. Independence is not particularly ideological. Instead, it is a commitment by the political system to tie its own hands to prevent the politicians who would otherwise be tempted to print lots of money to help themselves in the short run, at the expense of inflation, higher borrowing costs and economic instability in the long run. Presidents of one party routinely renominate Federal Reserve chairs picked by presidents of the other party, something that would be inconceivable with the more ideologically polarized Supreme Court.

One way the Fed maintains independence is that interest rates are set by the majority vote of a 12-person committee. Firing Powell would send a disastrous signal about Trump’s commitment to Fed independence, but it would be unlikely to actually lead to lower interest rates. The other 11 voting members of the Federal Open Market Committee would most likely never go along with Trump’s idea to cut the Federal Funds rate to 1 percent — and in fact would probably be even more reluctant to cut rates than they are now both to protect their independence and also because of the heightened concern about self-fulfilling higher inflation expectations in the new environment.

Even in the remote contingency that Trump somehow fired the entire committee and got a new group that agreed to lower interest rates, the new members would be able to lower only the rate controlled by the Fed, the Federal Funds Rate. This might matter to you if you are a bank in the overnight lending market. But businesses and households with mortgages borrow at very different interest rates, which are not controlled by the Fed but instead set by markets. And fears about the Fed’s independence would send markets into a tizzy with more risk and higher expected inflation almost certainly driving up longer-term interest rates.

A sustained and patient effort by Trump, however, could replace much or all of the Federal Open Market Committee members while indisputably following the letter of the law. At least two seats on the Board of Governors and usually more come open in every presidential term. Once a new group of members got control over the Board of Governors in Washington, they could use their leverage over the regional Federal Reserve Banks to ensure they picked only like-minded regional presidents. The next U.S. president could be dictating interest rates by the end of his or her first term.

Firing Powell would unleash a massive amount of uncertainty, litigation and market turmoil. But there would still be danger ahead even if that was avoided. Waiting 10 months for his term to end and replacing him with the wrong type of person could turn out even worse if President Trump and his successor were able to start the process of dismantling the independence of the group of people who, until now, have largely set rates based on their best (but not infallible) judgments of the good of the country, instead of the short-term interests of their own political party.

Comments